Mortgage Rates: Why Fed Rate Cuts Don’t Always Lower Home Loan Costs

Mortgage rates are a topic that is crucial for every home buyer and refinancer. There is only one question on everyone’s mind these days – if the Federal Reserve cuts its interest rates, will mortgage rates also fall directly? The reality is a little different. Mortgage rates are currently at the lowest point of 2025, but these rates are expected to remain quite volatile in the coming half. And the most interesting thing is that Fed rate cuts do not always have a direct impact.

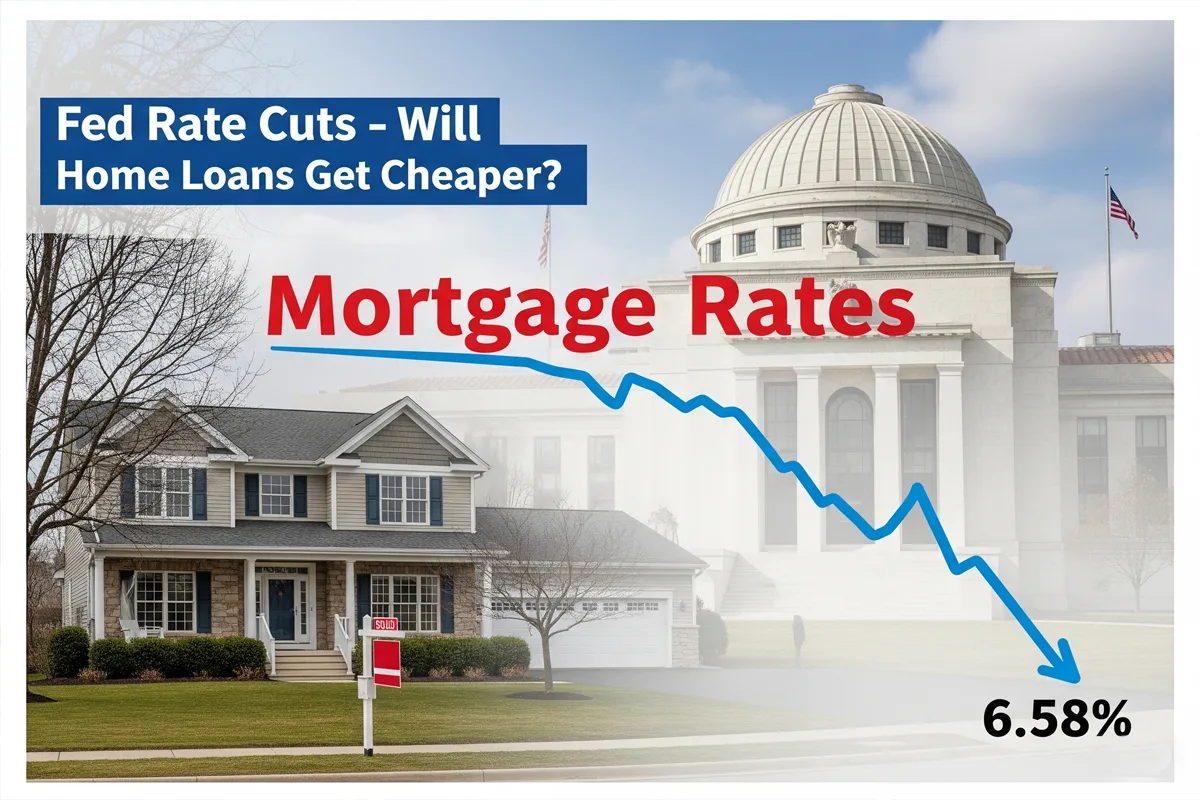

Mortgage Rates at Year-to-Date Low

This week, mortgage rates fell to 6.58%, the lowest level since October 2024. This decline has brought a ray of hope for buyers and refinancers. But experts are saying that the impact of the Fed’s next step has already been reflected in the market. Meaning, if the Fed cuts its benchmark interest rates in September, it is not necessary that mortgage rates come down further after that.

Why Mortgage Rates Don’t Always Follow Fed Cuts

Last year, when the Federal Reserve cut interest rates, mortgage rates had increased in reverse. It’s a strange paradox, but the reason is simple – mortgage rates are not directly tied to Fed rate cuts. In fact, mortgage rates are more closely linked to 10-year Treasury yields. Factors such as inflation expectations, government borrowing, and market volatility also influence mortgage rates more.

Homebuyers and Mortgage Industry Reaction

This is a frustrating time for mortgage industry professionals. All year mortgage rates were in the high 6% range, which made affordability tight and refinancing demand low. Now that rates are coming down, lenders are getting more calls from clients. But the problem is that many buyers still want to wait till September, thinking that there will be further decline after the Fed.

Mortgage loan originator Taylor Sherman shared his frustration on this matter – he said that buyers’ “wait till September” approach is wrong, because the market has already priced in the Fed’s action. That means if you are waiting for mortgage rates to fall further, you may miss that chance.

Fed Policy vs. Mortgage Rates

When the Fed cuts its interest rates, the impact is quickly seen on loans like credit cards and home equity lines, because they are tied to the prime rate. But standard 30-year fixed mortgage rates are not linked to prime rates. Sometimes it also happens that the Fed cuts and mortgage rates go up.

The main driver of mortgage rates is Treasury yields, and these yields depend on multiple factors – such as inflation expectations and investor demand. Along with this, mortgage spreads, i.e., the gap between the 10-year Treasury yield and mortgage rates, also play an important role.

What to Expect Next for Mortgage Rates

According to CME FedWatch, traders see about an 85% chance that the Fed will cut rates in September. But this has already been reflected in today’s mortgage rates. Meaning, it is not certain that home loan buyers will benefit further after the Fed’s decision.

Some crucial economic data is going to be released in the coming half, such as August hiring numbers, producer inflation, and consumer inflation reports. Mortgage rates fell to their lowest level last month due to weak jobs data. That means mortgage rates could go up or down in the next few half years, depending on new data.

Final Thoughts on Mortgage Rates

This time is a balancing act for homebuyers. On one hand, there is the possibility of lower mortgage rates; on the other hand there is market volatility and uncertainty. If you are planning to buy a house, then just waiting for the Fed’s next move may not be the best decision. It is more important to pay attention to the overall dynamics of the market and long-term affordability.

Disclaimer:

This article is written for informational purposes only. This is not financial advice. Mortgage rates constantly change according to market conditions. It is important to consult your financial advisor before buying or refinancing a house.

Also Read

US Economic Growth Slows but Shows Stability: Inflation, Jobs, and Retail Data Explained